Home Buyer 10 Commandments

Christel Renaud May 5, 2025

Christel Renaud May 5, 2025

🚫 What Not to Do When Applying for a Mortgage — and Why It Matters

When you're in the process of buying a home, your financial stability is under the microscope. As your loan officer, my job is to help you secure approval smoothly—and that means avoiding certain financial moves that can jeopardize your loan. Here’s why these are red flags for lenders:

Lenders verify your employment multiple times during the loan process. Changing jobs—especially switching industries or going from salaried to self-employed—can delay or derail your approval.

A new car loan increases your debt and affects your debt-to-income ratio (DTI), which is a major factor in qualifying. Even a zero-interest offer can impact your credit and loan eligibility.

The money you’ve set aside for closing must stay intact. If your account balance drops unexpectedly, the lender may see this as a risk and require updated documentation—or deny the loan.

Running up your balances can lower your credit score and increase your DTI. Even if you pay it off later, it may cause issues during the lender’s final credit check.

It’s tempting to furnish your new home, but buying items on credit before closing adds debt and can change your approval status. Wait until after closing.

When you co-sign, you’re taking on someone else’s debt—at least in the lender’s eyes. This can increase your financial obligations and affect your mortgage approval.

Lenders track your funds to ensure they're from acceptable sources. Changing banks or large transfers complicate the paper trail and can delay underwriting.

Always disclose all your debts. Lenders will find them anyway through your credit report, and omissions can create trust issues or lead to loan denial.

Any big deposit that can’t be sourced (like cash from a friend) raises red flags. Lenders need to know where your funds come from—especially when it comes to gift money or outside help.

Every inquiry impacts your credit score and can suggest financial instability. Opening new credit lines also alters your DTI and can trigger a re-evaluation of your loan terms.

Stability and transparency are key. If you're unsure whether something could affect your mortgage, always ask your loan officer before making a move.

📩 Need guidance on your home financing options? Let’s discuss your best path forward!

Christel Renaud | Christel Miami Luxury Living

954-799-3378 | [email protected]

Stay up to date on the latest real estate trends.

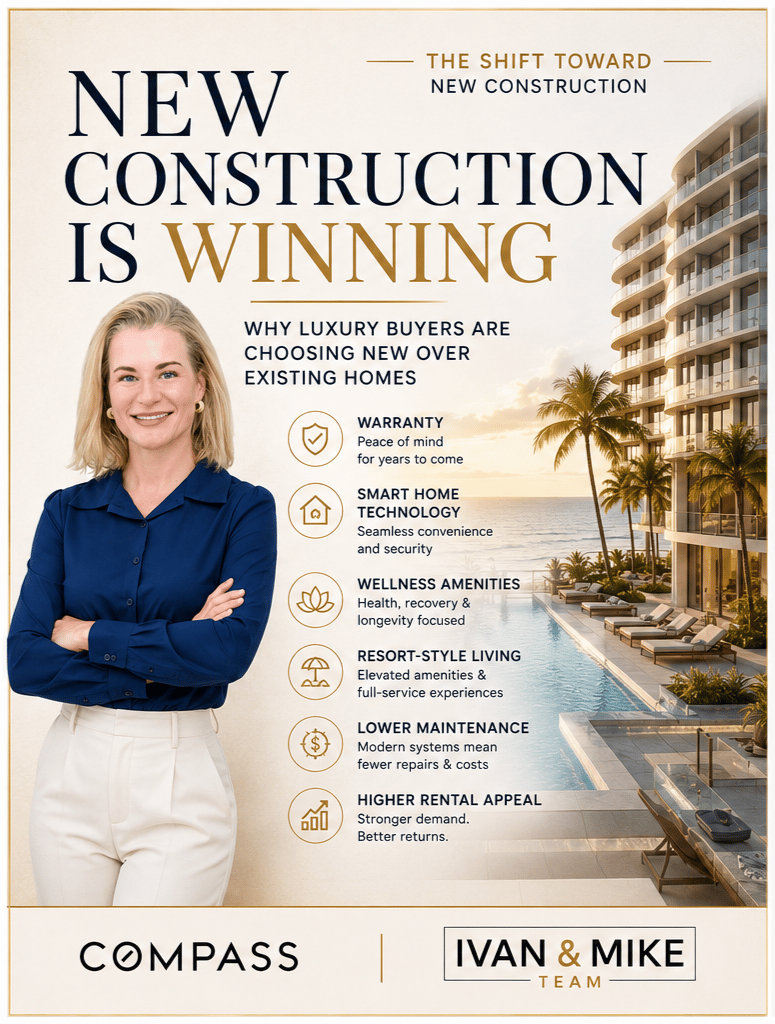

Why Buyers Are Investing In Lifestyle, Not Just Real Estate

Single-family home prices rise 31.8% year over year as inventory tightens and buyer demand remains active across Miami-Dade.

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact me today.