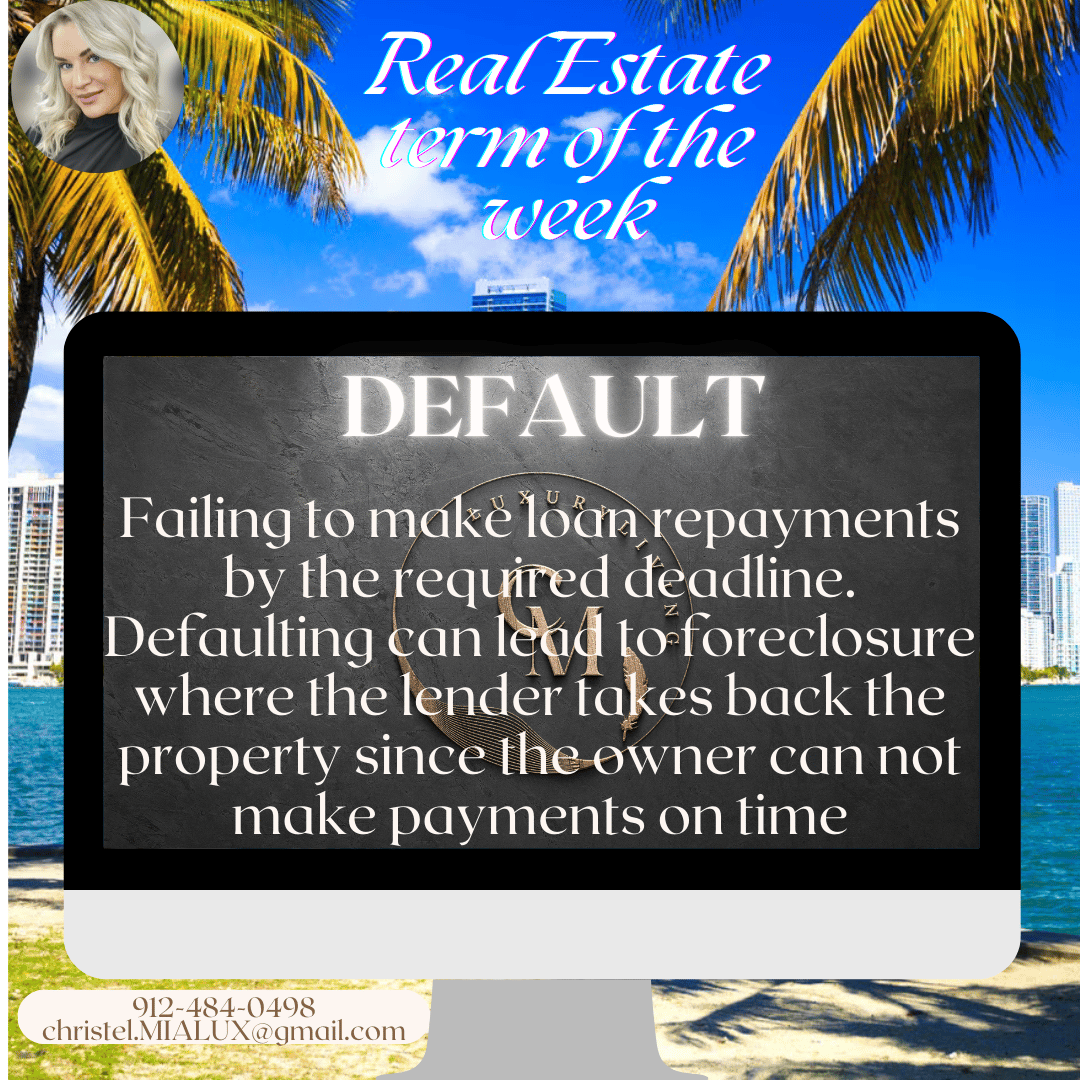

REAL ESTATE TERM OF THE WEEK - DEFAULT

Christel Renaud February 25, 2025

Christel Renaud February 25, 2025

Being in default on a mortgage is a serious situation, and it can have significant consequences for both your financial health and your homeownership.

Here’s why it’s bad:

Mortgage default will severely impact your credit score. A lowered score can make it harder to qualify for future loans, including other mortgages, car loans, or even credit cards. It may also result in higher interest rates if you’re approved for new credit.

If you’re in default long enough (typically 90 days or more), the lender may start the foreclosure process. This means the bank can take legal action to repossess your home and sell it to recover the money owed. Losing your home to foreclosure is a devastating outcome.

Defaulting can result in legal fees and additional costs, such as late payment penalties or collection fees. The longer you're in default, the more you may owe.

After a default, getting approved for a mortgage in the future can be extremely difficult. Lenders may be hesitant to lend to someone with a history of default, which limits your ability to buy another home.

The process of default and potential foreclosure can be incredibly stressful. It can lead to anxiety, feelings of insecurity, and uncertainty about your living situation, which can affect your overall well-being.

If the lender forecloses on your property, the sale may not cover the full amount you owe, especially if the market value of your home has dropped. You could be left with a deficiency balance, meaning you still owe money even after your home is sold.

For these reasons, it’s critical to address mortgage difficulties as soon as they arise—whether through refinancing, negotiating with the lender for a modification, or exploring other options like forbearance—to avoid the lasting negative impact of being in default.

If you are finding yourself about to be in default, please let us help you by connecting you with one of our approve lenders at no cost to you.

Christel Renaud | Christel Miami Luxury Living

954-799-3378 | [email protected]

Stay up to date on the latest real estate trends.

Panoramic Water Views Every Day

Why Branded Residences Are Redefining Luxury Living

Why Buyers Are Paying More For Space, Security & Exclusivity

WHY BUYERS ARE CHOOSING SMALLER LUXURY BUILDINGS

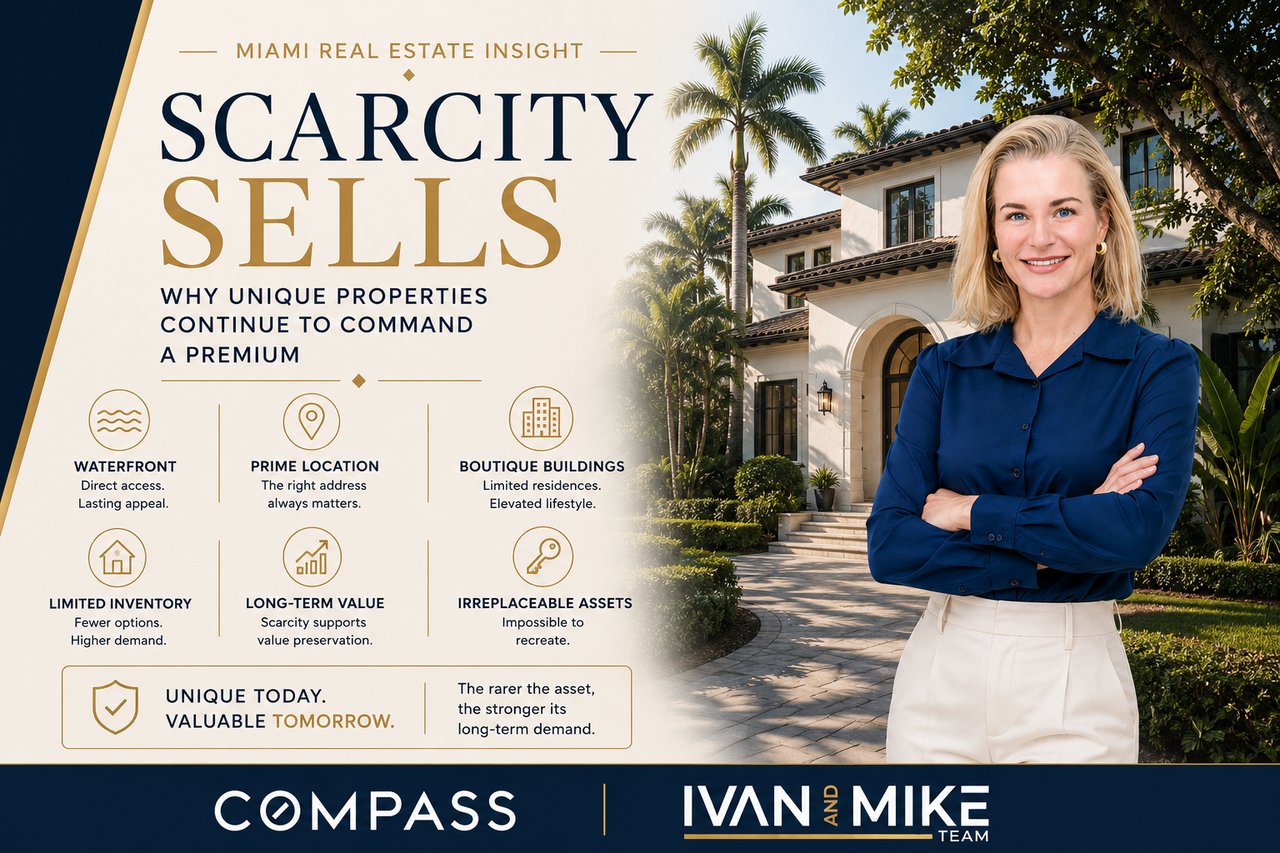

Why Unique Properties Continue To Command A Premium

Inside One of Bay Harbor Islands' Most Exclusive Waterfront Rentals

Why Buyers Are Investing In Lifestyle, Not Just Real Estate

Single-family home prices rise 31.8% year over year as inventory tightens and buyer demand remains active across Miami-Dade.

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact me today.